Case Study: Valerie

We’re fortunate to earn money when you click on links to products or services we already know and love. This helps support the blog and allows us to continue to release free content. Read our full disclosure here.

Welcome to our first case study!

Today we’ll hear Valerie discuss her budget and concerns in her own words. Let’s start with some month-to-month info.

Occupation: Graduate Student

Location: Portland, OR

Age: 23

Annual income: $20,000/yr

Typical paycheck: $950, but only $500 in the summer. I’m paid every other week.

Valerie says:

I’m a grad student trying to make ends meet. I feel like I really do not make much money, and it’s even less in the summertime. I can sometimes make extra through tutoring (I charge $20/hr), and I try to keep spending to an absolute minimum.

Biggest concerns: Having enough money for the essentials – rent, food, tuition. Yes, I pay tuition, but I get paid a stipend for teaching and research that more than covers it.

Sometimes I will put everything for the month on my credit card and pay that at the end of the month after I get paid.

Biggest goals: I’d like to pay off my student loans. I’m lucky I only have about $19,000 in loans but it’s still a lot of money. The fact that it will take me years to pay it down is discouraging.

Most proud of: Finishing my undergraduate degree in 4 years. I have friends who are still trying to finish!

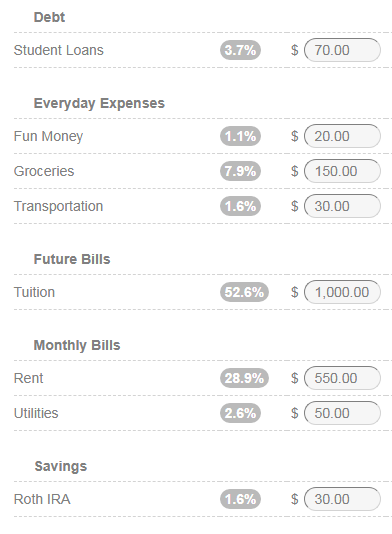

Tuition

My biggest expense is tuition. The stipend I get my from my research and teaching covers it, although money is really tight. When I finish out the year, I get 30% of it back. I’ll put that towards next year’s tuition so that I won’t have to use as much of my paycheck.

Student Loans

My student loans are still in deferrment while I’m in school (no interest, no payments required), but I want to pay off as much as possible anyway. Since they’re federal, not private, all of the rates are 6.5% or lower – I’m targeting the one with the highest interest rate, which is about $5,500.

Roth IRA

I do have money saved up for an emergency, which I keep in a savings account. I read online that 20-somethings should start saving for retirement ASAP. Since I don’t have a 401(k), I started a Roth IRA. I obviously can’t put in very much, but I set up automatic contributions for $30/month. I’m a little worried about how it will affect my taxes, but I’m sure it will be worth it!

Dang, that’s a tight budget.

Graduate students are famously underpaid and overworked. It’s easy to think of them as students living on their parents’ support, but the reality is that a graduate student will hit full-blown adulthood somewhere in their school days.

Many are married with kids. And kids are expensive.

Valerie is very fortunate to receive a stipend, since many students do not get paid while they pursue a graduate degree. It’s very easy for those folks to rack up even more debt on top of their undergraduate loans.

And student loans can be insideous.

Depending on how much debt you take on, the loss of income from delaying a career in industry might not cover the opportunity cost of staying in school.

Let’s take a fine-tooth comb to Valerie’s budget and see where she can improve.

Tutoring Hours & Rates

Valerie already mentioned that she sometimes tutors students for extra cash. While you do need to be careful that you’re not charging students for tutoring on the subject you’re actually a Teaching Assistant for, a TA can command a pretty high hourly rate.

At $40/hr, a measley 2-3 hours each week would total an extra $480/month.

Set your rates carefully.

It’s natural to want to charge less to entice more students – for example, $20/hr.

But you may wind up with a huge time commitment and not a lot of payout.

If Valerie increased her rates to $60/hr, she could earn upwards of $720/month for the same hours.

A general rule of thumb is to set your rate so that you look forward to the job. If you’re dreading every second of it, you might need to raise your rates.

You’d be surprised how much people value your time and skills – it’s easy to de-value your own skills because they don’t seem impressive to you, but someone else may be willing to pay top-dollar for them. You’ll never know unless you ask!

Additional income: $480.00

Beans & Rice

While $150 is already a beans-and-rice allowance for food – real beans and rice are cheaper than that. Grad school is famous for potlucks and meal shares. She may be able to save an additional $10/month by organizing batch meals with her colleagues.

That may not seem like much, but small amounts invested over time can have a huge impact. Over 50 years this habit could make you an extra $54,482.61 after kicking in only $6,000 of your own money.

Additional savings: $10.00

Roth IRA vs Student Loans

This is the age old question – should you pay down debt or invest?

Let’s get one thing out of the way: You should always be making the legal minimum payments towards your debt.

But assuming you have extra cash to spare – where should it go?

The math is actually surprisingly simple.

Pay toward whichever has the highest interest rate.

If you believe the stock market can net you an average return of 7% over the life of your account, and the highest interest rate on your debt is 6.5% – technically it makes sense to make the minimum payments on your debt and invest the rest.

If you have private loans (not federally backed), your interest rates may be much higher, and you’ll want to throw all of your money at that debt until it’s gone. While your savings rate will be nil in the short term, you will pay much less in interest over time and ultimately save more money.

That said, the decent plan you follow is better than the amazing plan that you don’t. If saving for retirement exictes you, do it!

We’ll stick with Valerie’s numbers on this one.

Adding It Up

There isn’t much room in Valerie’s budget – but she has a lot of income potential for a relatively low time commitment.

Total Additional Income: $480.00

Total Additional Savings: $490.00

Old Savings Rate: $30/$1,900 = 1.6%

New Savings Rate: $520/$2,390 = 21.8%

It’s not surprising that adding more money to Valerie’s budget would help tremendously, since her categories are so tight to begin with. The perfect time to start the saving habit is while your income is low, so that you can easily keep lifestyle inflation at bay.

If you’d like to share your budget with our readers, email us at hello@vermillion.app. We’d love to hear from you!

Related Posts

Case Study: George

Case Study: Nick