Why Socialism Belongs In Personal Finance

We’re fortunate to earn money when you click on links to products or services we already know and love. This helps support the blog and allows us to continue to release free content. Read our full disclosure here.

The economic landscape of America has been shifting under our feet for a while now. Your grandma may have been able to save today’s equivalent of $80 by sewing up a tattered shirt, but prices have changed.

In a lot of ways, consumer prices have fallen dramatically thanks to lower production costs. You can get a new shirt for less than $10, or free if you’re part of a Buy Nothing group.

Consider these massive changes:

- Cheaper consumer goods like clothes and food.

- New necessities such as internet, cell phones, and cars.

- Health, housing, and education prices have exploded.

And aside from these “home expenses” the average Joe now also has…

- High availability of credit and borrowed money.

- Digital banking and easy everyday investments.

- Privitized retirement investments.

Your grandma’s personal finance just isn’t going to cut it anymore.

Budgets are not enough.

Look, this is a budgeting website. We love budgets.

But a budget is a foundational tool. It’s only a part of the complete breakfast.

A budget can help you prioritize your dollars and save for what’s important, but it can’t decide what those important priorities are or help you get more dollars to put towards them. And if your priorities involve your health, your home, or your freedom – a budget is just not enough.

We may not like it, but these are broader economic problems. And unfortunately, they are also political issues. Socialism and personal finance can and should go hand-in-hand. But what does socialist personal finance look like?

A budget by itself is “rugged individualism” – it isolates you and implies that you can be completely self-reliant, independent from societal assistance.

But can you?

Should you?

Your Health

The average family spends almost $14,000 every year on health insurance. That’s right, just the insurance. Now add in co-pays, deductibles, and out-of-pocket expenses – Oh my!

So what do we do?

- Insurance premiums are automatically deducted from our paychecks.

- We set aside some cash for emergencies. (If we can.)

But what are we doing to lower the cost? What are we doing to increase the quality of our purchase?

Well, a lot of people are asking for a better healthcare system.

The Solution

This is socialized medicine – a universal healthcare system to provide for every citizen, subsidized by taxpayers, independent of employment.

But how would it impact your budget?

Instead of paying an insurance premium, you’d pay a bit more in taxes. And probably not a lot more than that. This in contrast to the thousands you’d be paying out-of-pocket if something happened to you now.

And you’d still have coverage if you lost your job.

How’s that for financial security?

Your Home

Homeownership is one of the main methods middle-class Americans use to build generational wealth. But if you don’t already own a home, it can be extremely difficult to break into the market without help.

If it’s not real-estate investment firms snatching up properties it’s rental moguls trying to make passive income. Or house-flippers.

Thanks for driving up the cost, guys.

And with favorable mortgage rates, competition is extreme – especially in good school districts. This drives up housing costs and makes cities unlivable for a large portion of their residents.

So what can we do?

The Solution

Housing-first policies, rent control, and public housing.

Where I live, these are the housing options:

- $1,500/month for an apartment

- $700/month for a room in a shared house

- $2,702/month for a house (if you’re lucky enough to buy one!)

Hope you don’t have kids, pets, or bad credit!

With more affordable housing options available, people would spend far less and enjoy greater freedom. Not only is that just plain savings, it also gives people more flexibility and leverage – and landlords less. This might even force costs down, since everyone would have viable alternatives.

Although rental properties are a large part of the FIRE movement, I personally have steered clear because it feels somewhat exploitative to me. Land is a finite resource, and every additional home I buy (and don’t live in) makes housing that much more unaffordable for those who make less than I do.

But that’s just me – you’ll need to find your own comfort level.

Your Freedom

Speaking of FIRE (Financial Independece/Retire Early), more people are embracing alternative employment – while others face incredibly difficult job market, with stagnant wages and dwindling benefits.

You don’t get unemployment benefits in the gig economy. (Except, maybe, possibly during Covid.)

You don’t even get vacation days.

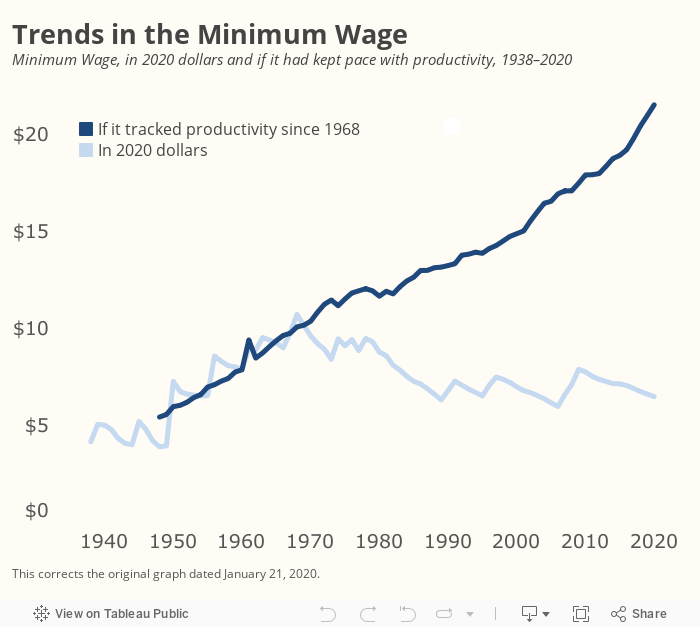

Income is becoming bimodal – that is, there are households making over $100,000/year that are doing relatively okay. And then there are households making less than $50,000, and they’re not doing so hot.

Accounting for inflation, we shouldn’t be fighting for a $15 minimum wage. We should be fighting for $24.

Now this is adjusted to keep pace with productivity, not inflation – but the result is obvious.

The poor will never be able to retire. Many have to work increasing hours just to keep pace with rising costs. And what’s worse – people have a hard time comprehending the size of the gap here.

The rich are richer than you think. We can absolutely afford higher wages.

The Solution

Raising the minimum wage will be a rising tide that lifts all ships – meaning you’ll likely make more at whatever job you do, even if you’re not making minimum wage.

And workers will have more money to spend, which will create more jobs. Good for the unemployed and good for business-owners.

Win win win.

In addition, we should fight for more progressive taxes to help fund social programs in a way that doesn’t penalize working class Americans.

More money and more social programs? Yes, please!

Put praxis in your budget.

Your politics don’t have to be perfect, but there are small ways you can incorporate socialism into your budget.

What does a socialist budget look like?

It supports your praxis.

After taking care of your living expenses, you should be looking toward the future and supporting causes that improve society. I call this being “selfish in the long run”, because you will absolutely benefit from living in a healthier, more robust society!

Here’s a list of ideas to help you get started. I recommend choosing one and putting in at least a few hours of effort every month.

Pick your praxis:

- Volunteer with mutual aide groups

- Join a socialist org to find out more ways to help

- Start or support a union campaign

- Start or support a worker co-operative

- Participate in local protests and pressure campaigns (joining an org will help with this!)

- Form or join a renter/tenant union

- Bring food to striking workers

- Donate to strike funds, nonprofits, etc.

Your praxis budget category.

Feel free to make a socialist budget category just to support your efforts. Or a praxis budget category. Any name meaningful to you will do.

Then put 1% of your paychecks in there.

Is 1% too much? Just put whatever you can.

Here’s how it might play out:

- Bring food to striking workers Money for groceries.

- Donate to strike funds, nonprofits, etc. Money for donations.

- Volunteer with mutual aide groups Money for childcare, providing you with extra time to volunteer.

At first it will feel strange and time-consuming but over time these efforts should give you a sense of fulfillment.

And while you work hard to lower your own cost of living, you’ll be helping those less fortunate by advocating for stronger social safety nets or providing direct aide.

If the goal of personal finance is to provide financial stability, then you’ll be right on track.

Because personal finance should be socialist.

Related Posts

Add A Category

Add A New Account